1. A Context of Gusty Winds

As the new geopolitical environment takes shape, Industrial Original Equipment Manufacturers (OEM) see how reading the context of their businesses has become more complicated. The existence of contradictory forces and the increase in pressure on the P/L, makes strategic decision making particularly complicated in the midst of uncertainty.

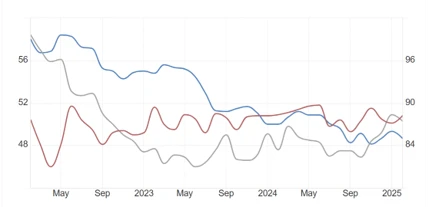

The decline of industrial optimism in Germany contrast with the improvement of the ISM Manufacturing PMI in the United States. (see A) Even China has seen a small improvement since the beginning of 2025.

But at the same time, diluting the particular complications of the Auto industry, the set of OEMs in Europe have demonstrated historical strengths (see B), which continue to attract the interest of global markets.

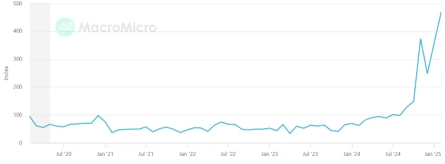

And yet the threats of custom tariffs materialize (see C), while new fears of inflation could put at risk the path of lowering interest rates, so important for CapEx-Intensive industries such as those of OEMs.

In this context, what sort of corporate strategy decisions should be on the Board check-list ?

MANUFACTURING SENTIMENT

(A) While German IFO (in blue) is at historical low, United States ISM Manufacturing PMI (in grey) seems to improve catching up with China’s Caixin Manufacturing (in red)

Source: Ifo institute, Institute for Supply Management and S&P Global

BUT EUROPE INDUSTRY AT HIGHS

(B) Despite conflicting forces, and diluting the effect of the European Car industry, the overall performance of OEM Industrial companies has demonstrated to be as a set strong. In the figure the STOXX Europe 600 Industrial Goods & Services

Source: Investing.com

AND AT THE SAME TIME WORLD TRADE UNCERTAINTY AT RECORD HEIGHTS

(C) And still linked to the new US Administration policy on international trade, uncertainty index is rocketing making it very difficult to know where to address the corporate strategy helm to cope with the new market conditions.

Source: IMF MacroMicro

2. Improving Revenue Stability

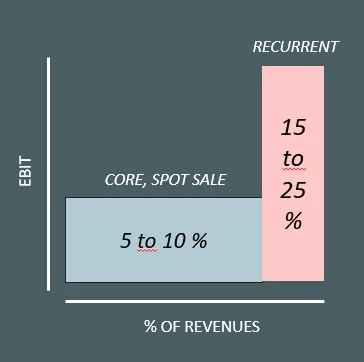

About ten years ago, at the same time that the new digital capabilities accelerated the transformation of business models, OEM companies started to gain additional interest in the idea of reinforcing the recurrent revenue, sometimes also referred as annuity, in the P&L.

The appealing is easy to explain, recurrent revenues like after-sale services, aftermarket parts or software licenses easily double or triple the level of profitability of core products themselves.

Today, in the new context of turmoil, the need for a structural stable base of annuity revenues is strategically even more important.

A higher degree of recurrent revenues will make the P&L more solid and resilient to the bumps and the potholes, but also it will change the value perceived by the client base and its loyalty.

Unfortunately, like anything good, it is not so easy to achieve. The new recurrent revenues will require new services, supply-chain traceability and new selling skills, among other things. These new capabilities will not sit idle in the company, it will imply a good assessment of what the company already have and what needs to be bought, whether it is in the form of “make” (IT projects) or “buy” (M&A).

Source: FdN

TYPICAL CAPABILITIES TO REINFORCE

Supply Chain Capability / IoT

New value added needs a really optimized supply chain, from forecasting to fulfilment, that with today’s IoT technologies uncover new service revenue areas for the OEM.

Digital Client Relationship

Digital client relationship is no longer an exclusive domain of the digital consumer, it is also key to gain fluidity on the B2B relationships.

AI-Service & Monitoring

The main uncover stream of recurrent revenues sits on the ability to monitor and service the lifecycle of the OEM products.

Sales Coverage & Dealers

Diversification is a great statistical source of stability on the revenue base. Turmoil times may be also good for stepping into previously complex areas or competitors.

Capital Solutions

Always minimised and often ignored the importance of proper capital solutions to speed-up sales, unlocking decisions and increasing global margins is paramount for the competing scenario.

Circular Economy

Circular economy is indeed about seeing new business opportunities in the after-market, while doing good for the ESG, and setting the pace from the OEM also in the area.

3. Carve-Outs: Gaining Agility

It is probably not in the ADN of the industrial OEM, which as investor tends to buy or build and keep the capabilities unless a really distress situation arrives. And still this vision of the industrial OEM as a stable investor continues to be the case in general. Nonetheless, the speed of change in the competitive environment leads eventually to do a step backwards just be able to gain inertia (funds) and jump forward three steps in the adjusted direction marked by the new strategy.

That implies often selling some good capabilities, which happen to be in the bad geography, or to play in no longer core technologies for the industrial group.

The feasibility of these “carve-out” operations increases with the emergence of new Private Equity investors that will see this as a great opportunity to seize the way of the carved-out division and dig deeper and further on its growth.

Of course that there are still some situations for distress and probably dismantle the value. But it is not on the mainstream of today’s Private Equity, which look primarily for stable and solid investments to make the expand, flourish and sell at a higher value.

Other Industrial groups, particularly local ones, will eventually show Interest in the new investment opportunity to gain local quota, reinforce their capabilities, or simply diversify.

In any of the cases, with new acquirers being Private Equity funds or Industrial Groups, Carve-outs are sometimes a necessary step to gain funds, get rid of unnecessary management time, and gain focus on the core of the new or adjusted strategy, that will probably go through more but different acquisitions in the desired domains and markets.

Turmoil times are also great for taking these decisions to show to shareholders, employees and partners a mastery of the OEM’s yellow path to achieve the OEM’s goals.

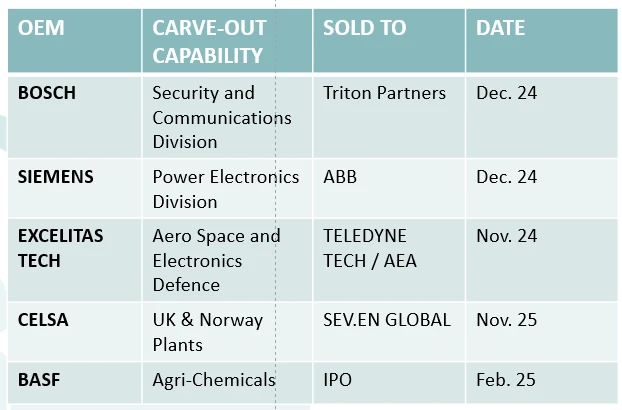

SOME CARVE-OUTS PERFORMED BY OEM's

A FOCUS GAME: MAIN REASONS FOR SELLING: FOCUS ON CORE ACTIVITIES AND/OR CORE MARKETS

4. Searching Speed of Growth

Once settled of any carve-out and ready to heap up for growth and to take advantage of the opportunities that any turmoil period arise, the Industrial OEM can look for ways of achieving and accelerating profitable growth.

With the right fit analysis and target definition of the required capabilities the mission is adding (or building, or both) another “Regional Champion” company/division in the Corporate Portfolio.

Fortunately, the industrial tissue of companies in Europe still contains sweet spots where the acquirer will eventually find the combination of 5 key sets of features:

1. Corporate, Technical and Cultural Fit.

2. Potential for organic business-as-usual growth.

3. Cross-border scale.

4. Consolidation opportunities.

5. Valuations out of the main street.

At FdN, our analysis of markets and experience, tells us that although being complex, it is not a unicorn to find; it is actually most of times feasible, and we have found it on several target companies crediting the convergence of the five set of elements.

THE FEU-DU-NORD 25 M&A CHECKS

-

Info-Memo analysis

-

Soundness of the seller’s BP. Breakdown. Sources and destroyers of value.

-

Commercial and operational synergies. CapEx requirements. 1st internal Business Plan.

-

Analysis of cash and WCR.

-

Analysis of assets and financial position. Internal plan on debt and capitalisation.

-

First Internal valuation (x & DCF). Range.

-

Risk and scenario analysis. Internal BP.

-

Human resources plan.

-

Final internal base model (Final - Iterated), EV + decision on Initial Offer Price and Deal Structuring.

-

Governance Plan

-

Competitive Analysis. Negotiation Process Governance/ Advisory.

-

Development of counter-offer (if required)

-

LoI - drafting/co-writing, negotiation, and agreement.

-

PMO due diligence.

-

Commercial due diligence

-

Accounting due diligence

-

Tax due diligence

-

Legal and social due diligence

-

HR due diligence

-

IT due diligence

-

Post-DD adjustments and agreement (if necessary)

-

Assistance with internal financing agreements (if necessary)

-

Share Purchase Agreement/SPA. Negotiations and drafts up to signature.

-

Advance preparation of the 90-day Plan and the PMI roadmap.

-

Quarterly support within the Monitoring Council/Committee.

KEY ELEMENTS FOR THE IDENTIFICATION OF ACQUISITION TARGETS

1. Corporate, Technical and Cultural Fit.

The first set of elements to define and influence the casting of potential targets are of course corporate and financial criteria (size, ownership, situation, etc.), technical capabilities sought after, and ideal cultural fit requirements

2. Potential for organic business-as-usual growth.

Despite turmoil (and even crisis) in some segments, there are a number of industries with double-digit demand growth forecasted for the next five to ten years, these tail winds will help achieving results independently of any other factors

3. Cross-border scale.

Whether tackled from the beginning or as a value strategy for the future, the potential synergies of scale (top and bottom of P&L) and better cross border client/dealer’s coverage, are must have criteria

4. Consolidation opportunities.

It is required an analysis of what we at FdN call the “Long-tail” profile, this will indicate the degree of consolidation and space for new leaders in the market segment and a good understanding of competition

5. Valuations out of the main street.

If possible, valuations will be outside the hot spot of the main street investors, this will make the approach not only more convenient but also less risky in terms of information asymmetry

5. How we help

MARKET STRATEGIES

Understanding markets and value creation dynamics is the essence of what we do. We only advise in verticals that we master and we start always by listening carefully to our clients. Our strategy thinking is always precise and fact based, sitting right in the center of the Board Agenda. We help with:

-

Strategy checks

-

Board memberships

-

Strategy Definition

FINANCIAL ADVISORY

Our Financial Advisory do not compare nor substitute accounting or transaction services. We will focus on the strategy of a transaction, the business plan, the scenarios and the valuation of it. We play the role of marking well the yellow road with side red lines for any transaction, making sure of governance and focus if required.

-

M&A approach, strat & valuation

-

Negotiation guide

-

Transaction governance

INDUSTRIAL PARTNERSHIPS

Despite difficulties, or precisely because of them, we know how to help on the choice and formation of Strategic Alliances and Joint Ventures, typically for achieving Capital Solutions, Market Reach, or Winning Tenders.

-

Strat Alliances guide

-

Tenders in co-operation

-

Public-Private Partnerships

INVESTMENTS

We cast, facilitate and guide the collaboration between industrial players and private investors, choosing carefully the right fit, to enable successful investments and long-lasting business relationships.

-

Private Equity Investments

-

Corporate Venturing advisory

-

Indirect-Influence strategies